How to Open a “Trump Account” for Your Child: A Step-by-Step Guide

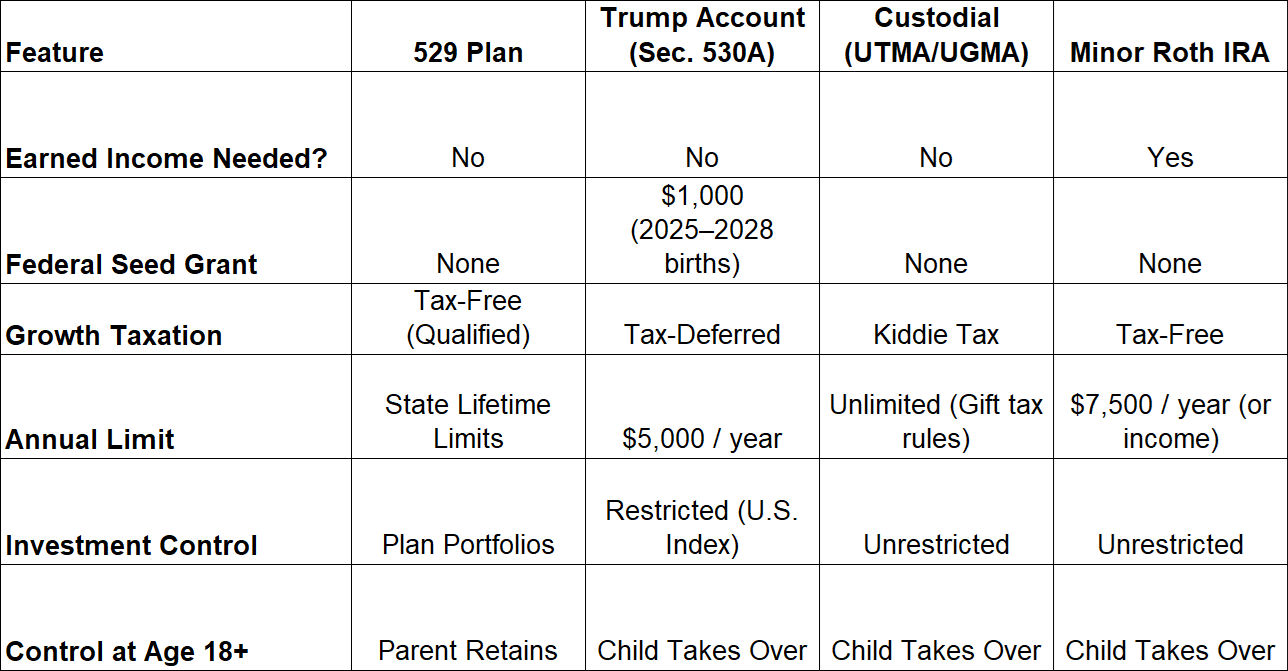

If you are looking to build long-term wealth for a child in your life, Section 530A Trump Accounts offer a unique way to start early. Created under the One Big Beautiful Bill Act (OBBBA), these accounts act as a pre-funded starter retirement account for kids under 18, complete with a $1,000 federal seed grant for eligible children born between 2025 and 2028.

While Trump Accounts work similarly to traditional IRAs in the long run, the process of opening and managing one is slightly different from setting up a standard brokerage account. Here is a straightforward walkthrough of how the process works and what to expect at each step.

Step 1: Submit IRS Form 4547 to Register

Unlike opening a regular bank or investment account, opening a Trump Account starts directly with the federal government.

To get started, an authorized adult—usually a parent or legal guardian—must file IRS Form 4547 (Election to Establish a Trump Account). This form registers the child as the account owner and allows you to claim the $1,000 federal grant if your child qualifies.

You can submit Form 4547 in one of three ways:

-

Online via the IRS: Through your official IRS Online Account.

-

On Your Mobile Device: Through the official Trump Accounts mobile app.

-

With Your Tax Return: Filed alongside your annual federal income tax return.

Step 2: Activate the Account Online

Once the IRS processes and approves your Form 4547 submission, you will receive confirmation to activate the account.

-

Where to Go: Head to the official portal (

[www.trumpaccount.com](https://www.trumpaccount.com)) or open the Trump Accounts app to complete activation. -

Central Administrator: Currently, Robinhood serves as the central platform for initial account creation and administration.

-

Future Portability: While you must open and activate the account through the central system first, options to transfer or roll over the account to other financial institutions are expected to open up in the future.

Step 3: Fund and Choose Your Investments

Once activated, you can begin contributing funds and setting up your investment strategy:

-

Contribution Limits: Family, friends, and even employers can contribute up to a total of $5,000 per year in after-tax dollars. The child does not need to have earned income to receive contributions.

-

Employer Match: Employers can contribute up to $2,500 per year toward the $5,000 annual limit.

-

Investment Options: Prior to age 18, investments are kept straightforward. Funds are invested in broad-market U.S. index options, such as funds tracking the S&P 500.

Tax Tip: Keep good records of the personal contributions you make! Private contributions go in using after-tax dollars, whereas government seed funds and market growth are pre-tax. Good record-keeping helps ensure your child isn’t double-taxed on those contributions when they make withdrawals years down the road.

Step 4: What Happens When Your Child Turns 18?

During childhood, you control and manage the account as the parent or guardian. However, on January 1st of the calendar year your child turns 18, a few key shifts happen automatically:

-

Conversion to a Traditional IRA: The account officially transitions from a Trump Account into a standard Traditional IRA.

-

Transfer of Ownership: Full control and administrative responsibility pass directly to your child.

-

Investment Freedom: Your child can expand their investments beyond broad index funds into individual stocks, bonds, or other asset classes.

-

Standard IRA Rules Apply: Withdrawals before age 59½ generally face a 10% penalty plus ordinary income tax, though standard IRA exemptions apply (such as using funds for higher education tuition or a first-time home purchase).