HIGHLIGHTS

- US and international stocks were up by 2.05% and 1.69% but oil falls hard (-7.95%).

- The first debate marks a new low in presidential politics.

- Trump tests positive for Covid.

- Payrolls increase by 660k but that was short of estimates.

- Consumer confidence jumps higher.

- This will be a record year for retail store closings.

- More layoffs announced.

- A dreary long-term forecast by the CBO

MARKET RECAP

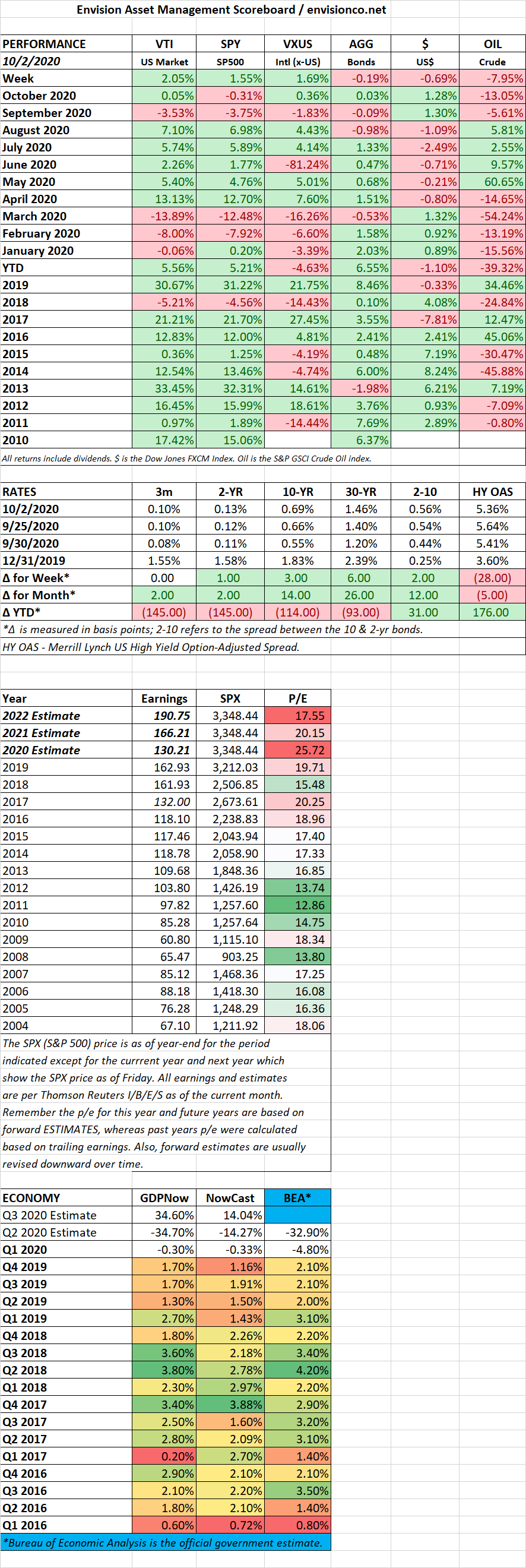

US stocks were up by 2.05% and international stocks were 1.69% higher on hopes for a stimulus bill. Oil slumped by 7.95% on fears of a slowing economy.

Trump and Biden faced off in the first Presidential debate on Tuesday and let’s just say there was nothing presidential about it. It was a new low in presidential politics as Trump just talked over and through the moderator and Biden. Then on Friday, it was announced that Trump had tested positive for Covid. Analysts seem to think this increases the odds of a stimulus bill.

Payrolls were up by 661,000 in September. Leisure and hospitality began to come back to life, adding 318,000. Construction was also strong, plus 26,000. But the total number was 200,000 lower than the consensus estimates. The unemployment rate fell to 7.9% from 8.4% last month, but a lot of that was driven by the fact that 700,000 people left the workforce. Payrolls are still 10.7 million less than the February numbers.

The Conference Board reported that consumer confidence jumped to 101.8 in September from 86.3 in August. It was the biggest increase since April of 2003 and brought the index to the highest level since March. Consumer confidence had dropped in the two previous months due to Covid outbreaks in several states like Florida and California.

A record number of retail stores are closing and will set a record by year-end. Through mid-August, more than 10,000 stores have either closed or there have been announcements that they will close, and that number could shoot up to 25,000 by year-end according to market-research firm Coresight Research. That tops the 9,500 from last year. Six thousand of those closings were due to bankruptcies. That translates into 130 million square feet of space. More than half of that is due to JC Penny, Stein Mart, Bed Bath & Beyond, and Pier I Imports.

US household income fell by 2.7% in August due to a drop in unemployment benefits. Despite the drop, household spending was up by 1% in August, down from 9% in May, 7% in June, and 2% in July. Initial jobless claims fell by 36,000 to 837,000 for the week ending September 26. American Airlines and United plan to proceed with 32,000 job cuts, other job cuts announced were 3,800 by Allstate and 28,000 by Disney.

The long-term growth forecast for the US, released last week by the Congressional Budget Office, is dreary at best. The CBO projects economic growth to average 1.6% over the next three decades. The lowest number since the 1930s. The slow-growth is a result of demographics, productivity, and national debt. Covid has impacted birth rates this year and probably going forward. That, combined with less immigration, and already falling birth rates, means less young Americans to help grow the economy in the future. Productivity is projected to slow due to less business investment and an older population. Exploding national debt will crowd out private investment. The CBO projects that in 2049 debt will be 189% of GDP, from 79% last year.

SCOREBOARD