MARKET RECAP

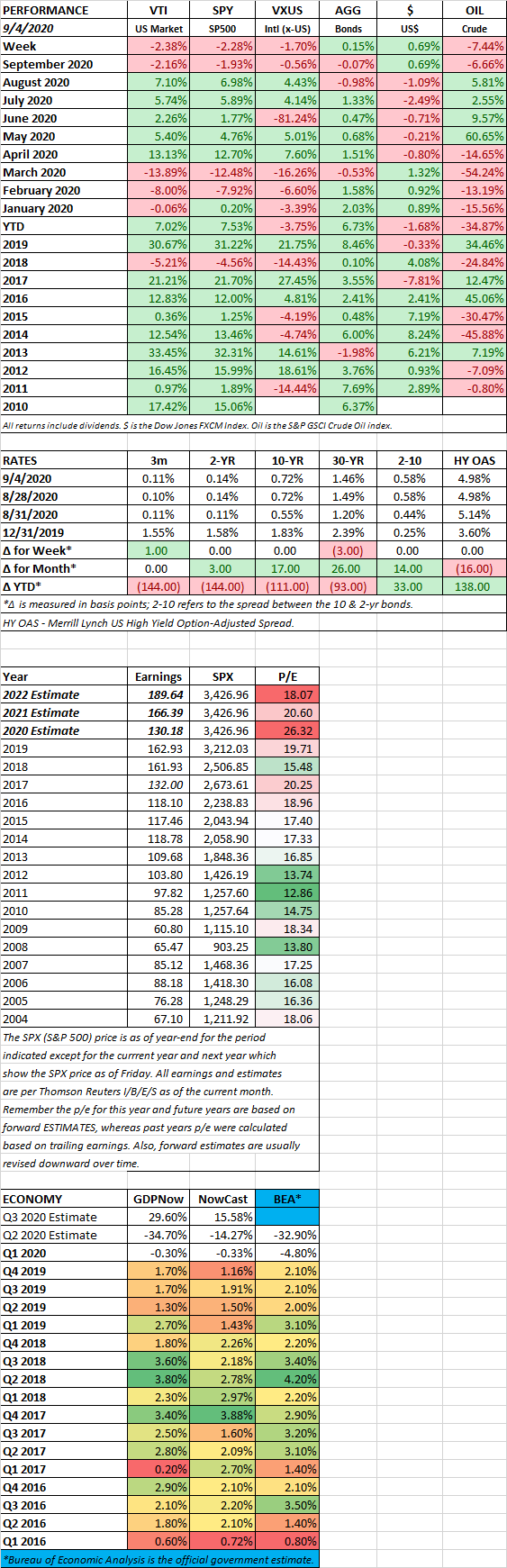

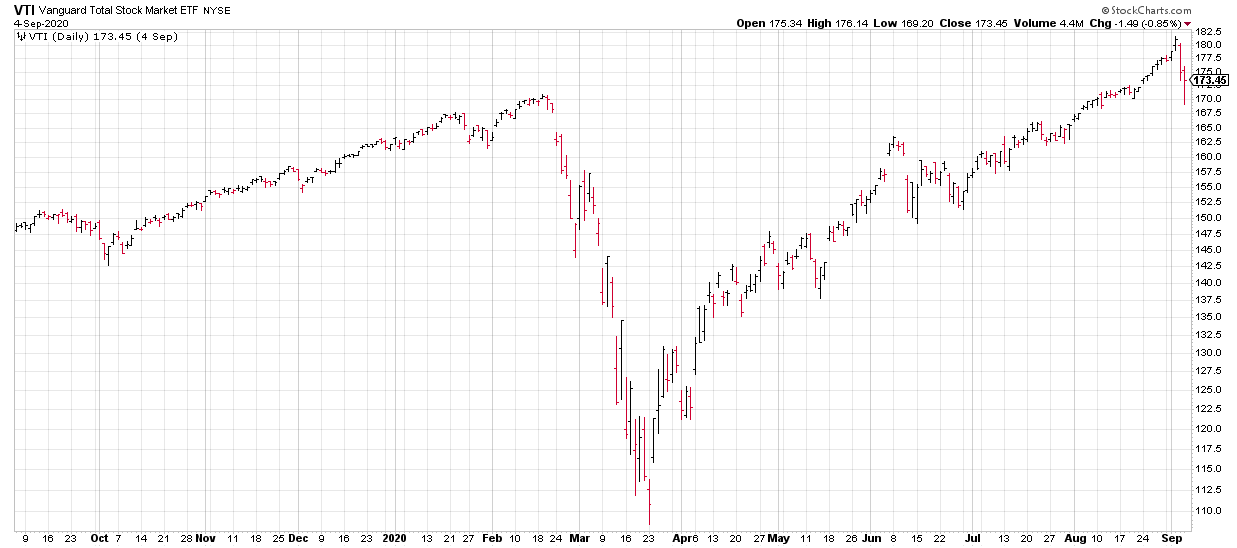

US stocks fell by 2.38% and international stocks were down by 1.70%. The decline ended five consecutive weeks of gains. The S&P 500 is up 35% since April, it best run since 1938. The big hit was on Thursday and Friday when the market fell by 4.3% or $1.7 trillion in market cap. From the Wednesday high to the Friday low, the decline was 6.9%. However, the decline was just a small dent in the market rally, but a big fall like that can sometimes be a signal that more is on the way.

Unemployment fell to 8.4% in August from 10.2% in July as employers added 1.4 million jobs in August. It was a very strong employment report but doesn’t factor in recently announced layoffs that are on the way (see our commentary last week).

US debt has now reached the highest level since WWII. Federal debt held by the public will exceed 100% of US gross domestic product, putting the US in the same position as only a few countries around the world, including some economic “powers” like Italy and Greece. The last time US debt exceeded the GDP was in 1946 after years of financing WWII. The borrowing though has not slowed down investors, who still are happy to purchase treasuries that yield almost nothing. With ultralow interest rates, the government can get away with this, for now. Under the assumption that the US does not deal with the debt issue, it won’t be a problem until it becomes a problem, that being when the market pushes interest rates higher, or the government is forced to suppress interest rates even more than they are now leading to all kinds of unintended consequences. That may be a year from now or fifty years from now.

SCOREBOARD