HIGHLIGHTS

- US stocks were down by 2.38% and international stocks dropped by 1.80%.

- Negative technical signs for US equities.

- Only 20,000 jobs added in February.

- Interest rate policy turns dovish worldwide.

- The deficit is really exploding.

- Tariff costs are being borne by US consumers.

MARKET RECAP

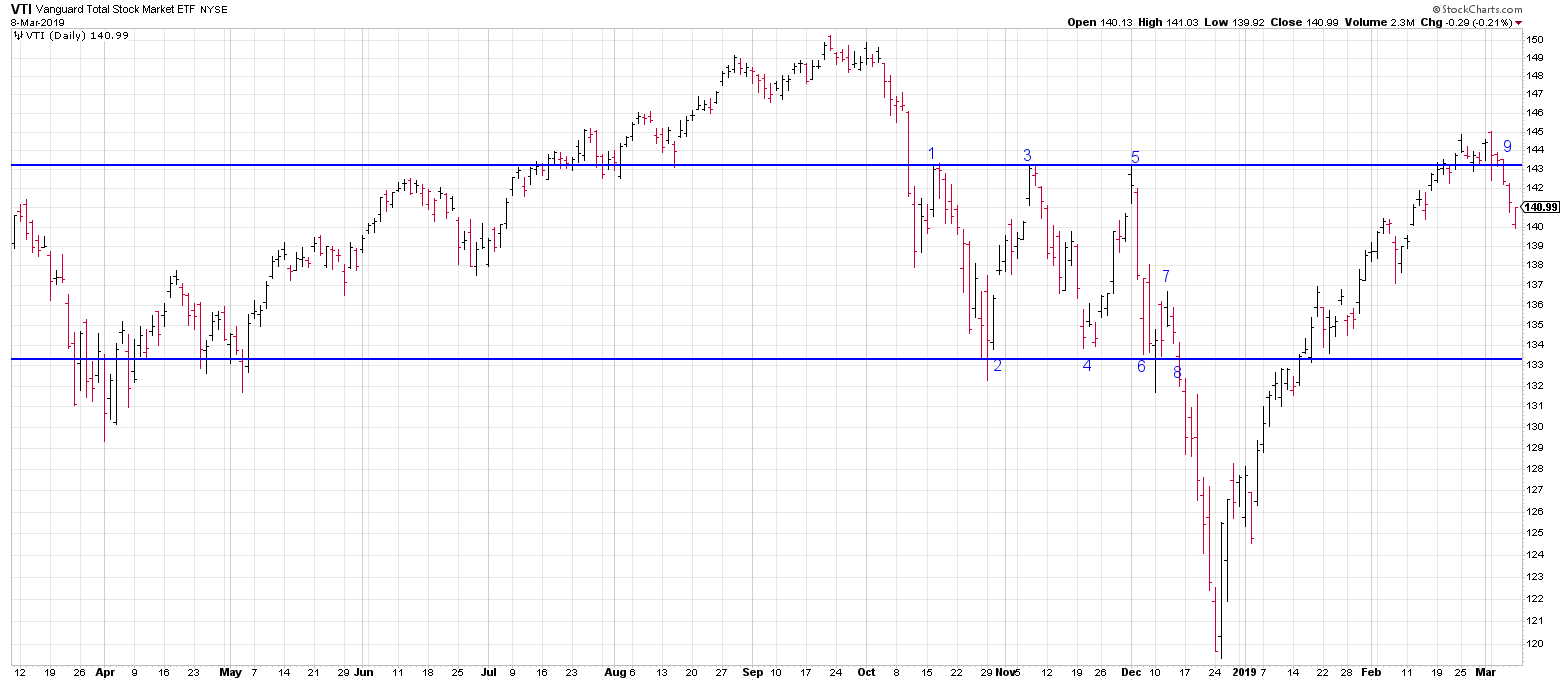

Stocks fell by 2.38% in the US and 1.80% x-US. Bonds advanced by 0.75%. US stocks fell below their 200-day moving average. Looking at a chart of the VTI (total stock market), last week prices broke through the resistance level set at points 1, 3, and 5 (see chart below) from the 4th quarter of last year, but this week they could not hold that level and fell back below the resistance line (see 9). That is what technicians call an “upthrust”, when a stock or fund moves above resistance and then quickly reverses and moves back below resistance. The upthrust move and dropping below the 200-day average are negative technical signs. Stocks were in an overbought condition, so a sell-off is not a big surprise, so far it has been mild. We showed a couple of weeks ago a similar set-up in 2011 to the current market when stocks dropped 10%. But the market constantly surprises so anything can happen.

PAYROLLS

Only 20,000 jobs were added in February, the weakest report since March of 2011, assuming future revisions don’t change it. There is some belief that there are errors in the data as a result of the government shutdown. Taking 20,000 as a stand alone number, the report looks weak. However, if you look at the last 2 or 3 months as an average, the numbers look healthy. The unemployment rate decreased to 3.8%. Year over year, average hourly earnings were up by 3.4%.

INTEREST RATES

In the span of just a few months central bank interest rate policy has turned dovish worldwide. The ECB downgraded its forecast for Eurozone GDP growth from 1.7% to 1.1% for 2019. They now plan to keep interest rates at current levels through the end of the year. That is longer than was originally planned. The ECB also said they would begin issuing inexpensive long-term loans in September and the program would run through March of 2021. China has also begun issuing loans to companies to promote growth. This follows the Feds announcement that they would put the breaks on interest rate increases for the time being. In a low-interest rate world, equities generally become more attractive.

DEFICIT

The US government deficit soared by 77% for the first four months of the fiscal year to $310 billion. Federal outlays were up by 9% and receipts were down by 2%. The outflow was due to higher spending on the military, veteran affairs and interest on the debt. Receipts fell because of lower corporate and individual income-tax collections. Keith Hall, Director of the non-partisan Congressional Budget Office (CBO) said: “It’s hard to imagine this is sustainable.”

Beginning in 2022, the CBO expects deficits in excess of $1 trillion and will average 4.4% of GDP, compared to 2.9% in the previous 50 years. Expect tax increases in the next few years.

TARIFFS

A study by economists has pegged the cost of the US trade tariffs to consumers at $69 billion. That counters the White House argument that the cost of the tariffs are paid for by foreign countries. Overall, combining costs and benefits, the tariffs have cost the US economy $6.4 billion. The Centre for Economic Policy study stated that “We find that the U.S. tariffs were almost completely passed through into U.S. domestic prices.”

Tariffs have also impacted world trade, leading to a slowing global economy. Chinese exports fell by 20.7% year over year in February and auto sales dropped by 18.5%.

SCOREBOARD

Past performance does not guarantee future results.

The purpose of this commentary is to provide readers with a summary of recent market and economic news. It is not intended to provide trading advice. Investors should have a long-term plan and should consider working with a professional investment advisor. Any discussion of investments and investment strategies represents the presenter’s views as of the date created and are subject to change without notice. The opinions expressed are for general information only and are not intended to provide specific advice or recommendations for any individual. The information and opinions contained in this material are derived from sources believed to be reliable, but they are not necessarily all inclusive and are not guaranteed as to accuracy. Any forecasts may not prove to be correct. Economic predictions are based on estimates and are subject to change. Reliance upon information in this material is at the sole discretion of the reader.