MARKET RECAP

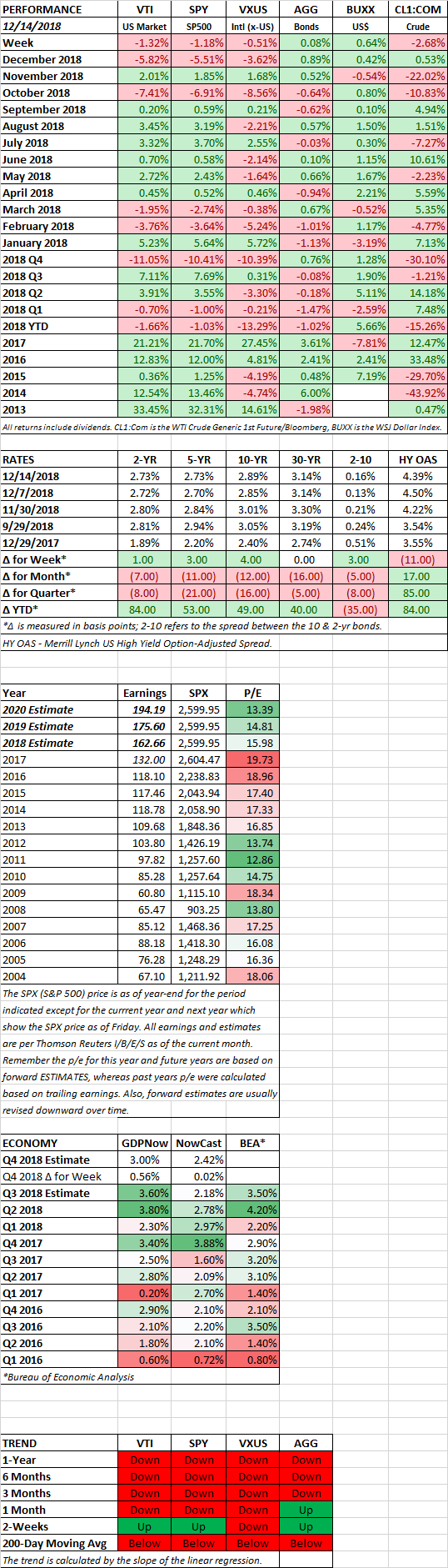

It was another bleak week on Wall Street, stocks slid by 1.32%, which sounds almost mild by recent standards, but from midday Wednesday on, stocks gave up positive gains from Monday and Tuesday. International equities fared slightly better, falling by 0.51%. And bonds were up by 0.08%. The S&P 500 closed at its lowest level since April, the index is down by 11.28% since its high on September 20th.

Economic news was weak overseas but positive in the US (see further below). News that the US might be headed for a government shutdown hurt markets. Trump wants to build his wall for $5 billion but Democrats have offered $1.3 billion. Trump says he will shut down the government until he gets funding for the wall. Trump’s former lawyer Michael Cohen was sentenced to three-years in prison and a federal investigation was opened into whether the Trump inauguration committee spent funds illegally.

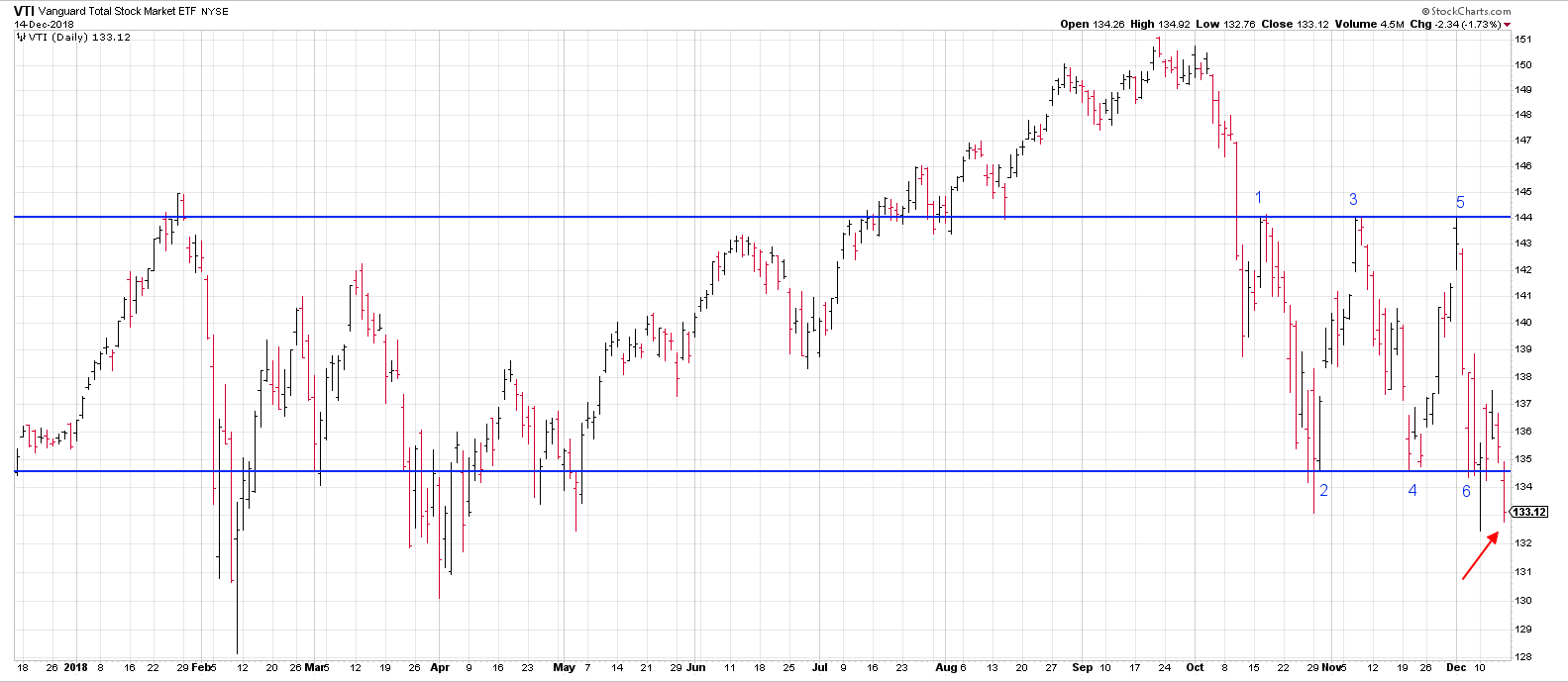

The VTI (US Total Stock Market) fell just below the support line we marked last week. See the red arrow below. Indicating a higher chance of another leg down.

ECONOMY

The debate rages on if a recession is knocking at the door, as in the next year or so. Outside the US, economies have been on stall speed for a while and might be getting worse. China reported that industrial production had slowed to its weakest point, +5.1%, since early 2016. The growth in retail sales in China, +8.1%, fell to the lowest level in 15-years. Note the numbers in China are still positive, but slower than what they are used to.

In Europe, Italy is close to a recession and in France, anti-government protests have resulted in a drop in business activity for the first time in two years. In England, the Brexit mess is hurting economic activity. The composite purchasing managers index for the Eurozone fell to 51.2 from 52.7, still indicating growth (greater than 50) but clearly slowing down.

The US is in better shape, but the forecast is for slower growth compared to recent quarters. The IMF projects 2.5% growth in the USA compared to 3.5% in Q3 and 4.2% in Q2. However, economic reports that came in this week were positive, and the Atlanta Fed’s GDPNow model upped its estimate of Q4 growth to 3.0% from 2.44% last week.

November retail sales beat expectations. Sales were up by 0.2% versus an expectation of 0.1%. Excluding autos and gas, sales increased by 0.5% versus 0.4%. Online sales increased by 2.3%. Gas stations fell by 2.27% on lower gasoline prices.

Industrial production increased by 0.6% in November after falling 0.2% in October. Year-over-year, industrial production was up by 3.9%.

Unemployment claims dropped for the week to 206,000, much lower than forecasts and significantly lower than the two previous weeks.

BARRON’S COVER STORY

Amidst all the gloom, Barron’s cover story is titled “Why stocks could rise more than 10%” in 2019. Based on interviews with 10 strategists, the group has an average projection of an increase of 14%. Earnings on the S&P 500 are expected to rise by 5% to $172 per share, the strategists are mildly optimistic that US and China will reach a trade deal at the beginning of the year, interest rate increases should slow, and GDP should grow by 2.5%. A primary risk to the forecast is a breakdown of talks between the US and China.

STOCK VALUATIONS DROP TO FIVE-YEAR LOWS

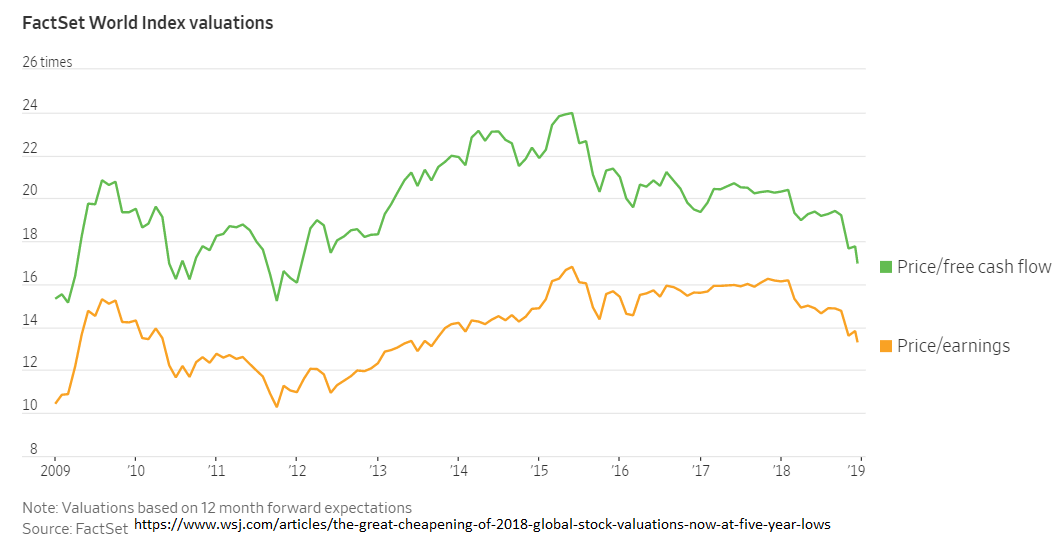

International equity valuations are hitting five-year lows. According to FactSet, the forward price-to-earnings ratio is now at 13.3, down from 16 earlier in the year. The price-to-free cash flow ratio is at the lowest level in six years. While these valuation ratios are falling, earnings for companies in the FactSet World Index are expected to rise by 16% over the next year. Higher interest rates might account for some of the drop in valuations, as well as worries about slowing economies around the world.

CHINA TO OPEN MARKETS

It was reported on Wednesday that China was going to adjust their industrial policy so that it becomes friendlier to foreign businesses. China would back off their policy to become the world leader in technology and manufacturing by 2025 and the country would become more open to foreign companies. Tariffs will be lowered on auto imports and China would increase their purchases of US agricultural products.

SCOREBOARD

The purpose of this commentary is to provide readers with a summary of recent market and economic news. It is not intended to provide trading or investment advice. Investors should have a long-term plan and should consider working with a professional investment advisor. Any discussion of investments and investment strategies represents the presenter’s views as of the date created and are subject to change without notice. The opinions expressed are for general information only and are not intended to provide specific advice or recommendations for any individual. The information and opinions contained in this material are derived from sources believed to be reliable, but they are not necessarily all-inclusive and are not guaranteed as to accuracy. Any forecasts may not prove to be correct. Economic predictions are based on estimates and are subject to change. Reliance upon information in this material is at the sole discretion of the reader.