HIGHLIGHTS

- The markets took a tumble as US and international stocks fell by about 4%.

- Interest rates moved significantly higher.

- The sell-off has been way overdue.

- A strong jobs report shows the economy is in good shape.

- And earnings estimates continue to be high.

MARKET RECAP

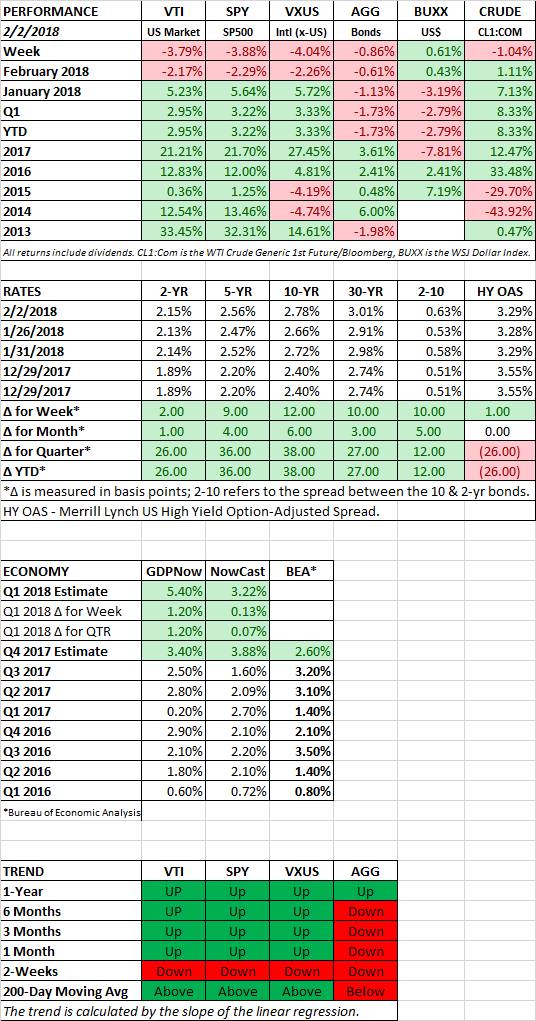

The equity markets took a tumble around the world. US stocks dropped by 3.88% on the week and international stocks fell by 4.04%. The longest streak of all-time without a 3% sell-off ended at 448 calendar days.

Fast increasing interest rates put an end to the rally. The 10-year treasury bond now yields 2.78%, the most since January of 2014. The 30-year cracked the 3% barrier, closing at 3.01% on Friday.

Higher interest rates are having a gravitational pull on the price/earnings ratio, bringing it down. The problem is not earnings, earnings estimates continue to be strong. It is the amount that investors are willing to pay for those earnings have declined, resulting in the sell-off

Why are interest rates going higher? Ironically good news in the economy means higher wages which translates into higher inflation. The worst day of the week was on Friday after a strong jobs report that showed the biggest increase in wages since June of 2009 (see below). In other words, the good economic news was bad market news.

There is also the impact of the unwinding of the balance sheet. As the Fed lets bonds mature, it is effectively taking money out of the system. That means less demand for bonds which requires higher rates to entice investors.

There are other forces at play also. The biggest one might be that we were just due for a sell-off. Not just due, but way overdue. It has now been 585 calendar days since the last 5% sell-off. That is just 8-days shy of the all-time record which occurred between December of 1957 and August of 1959. There was also extreme positive sentiment in the market. Volatility has been at all-time lows, indicating almost no fear of a sell-off.

And then you have the political mess in Washington. Investors and traders simply ignored our dysfunctional political system while the market was in a one-way mode up, but that will be harder now. The release of the Republican memo alleging surveillance abuse, despite the objections of the Justice Department and the FBI, indicate that our political mess is getting worse, not better. And let’s not forget that the government has until Thursday to continue to fund the government before the next shutdown.

So, we have what is likely the beginning of some kind of sell-off. Whether it ends on Monday or continues on for a while we have no way of knowing, but we suspect it will go somewhat deeper. This is part of normal market behavior. There is no sign, at least now, of a recession soon, and the economy and earnings estimates are solid.

JOBS

Nonfarm payroll increased by 200,000, the preceding two months were revised downward by 24,000. Average hourly earnings were up by 0.3% month over month and 2.9% year over year. That was this biggest increase since June of 2009 and might have led to higher inflation fears that spooked the market during Friday’s selloff. The average workweek fell to 34.3 from 34.5 hours. The unemployment rate remains at 4.1%.

GLOBAL ECONOMY

The global economy continues to be in solid shape. The manufacturing PMI came in at 54.4, down 0.1 point, but a strong number. Anything above 50 is considered expansionary. 94% of countries are in expansion territory, close to the November high. But it appears that growth in PMI is leveling off.

HEALTHCARE ALLIANCE

Amazon, JP Morgan, and Berkshire Hathaway announced they would join forces to try to tackle the problem of healthcare costs.

SCOREBOARD