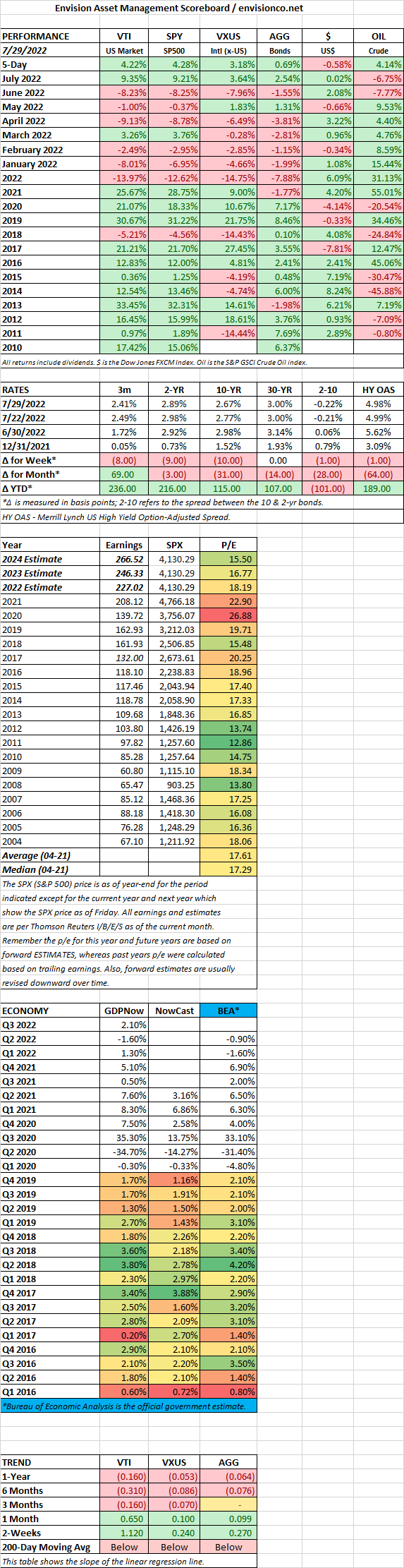

MARKET RECAP

The S&P 500 fell by 20.6% for the first six months of the year. At the time, we wrote, “the market has fallen at least 15% in the first six months of the year in 1932, 1939, 1940, 1962, and 1970, down by an average of 24.7% in those years. But stocks rallied in the back half of those years by an average of +21.2%.” At least so far, true to form, stocks went into rally mode, the S&P 500 gained 9.1% for July, the best performance since November of 2020. The monthly performance was helped by an ultra-strong week, US stocks were up by 4.2% and international stocks by 3.2%. Bonds increased by 0.69% as interest rates continued to fall.

Investors are counting on the old bad news is good news mindset. A slowing, or declining economy, means interest rates don’t need to rise as much, and interest rates cuts would happen sooner than expected. Also earnings have not been as bad as feared.

But it is still too early to call the all clear. There have been plenty of times when markets have gone back to test the lows, or even break them. Inflation is not done yet, the economy just banked two successive quarters of declining growth, with no clear signs of an economic pickup. Cutting interest rates too soon would be out of the 1970s playbook, a strategy that didn’t work so well in fighting inflation.

GDP declined by 0.9% in the second quarter. That marks the second straight quarter of declining GDP, the unofficial sign of a recession. Wages and benefits increased by 5.1% in the second quarter, compared to a year earlier, but that was short of the 9.1% increase in consumer prices. The wage and benefit increase was the most ever, since they started keeping records in 2001.

SCOREBOARD