MARKET RECAP

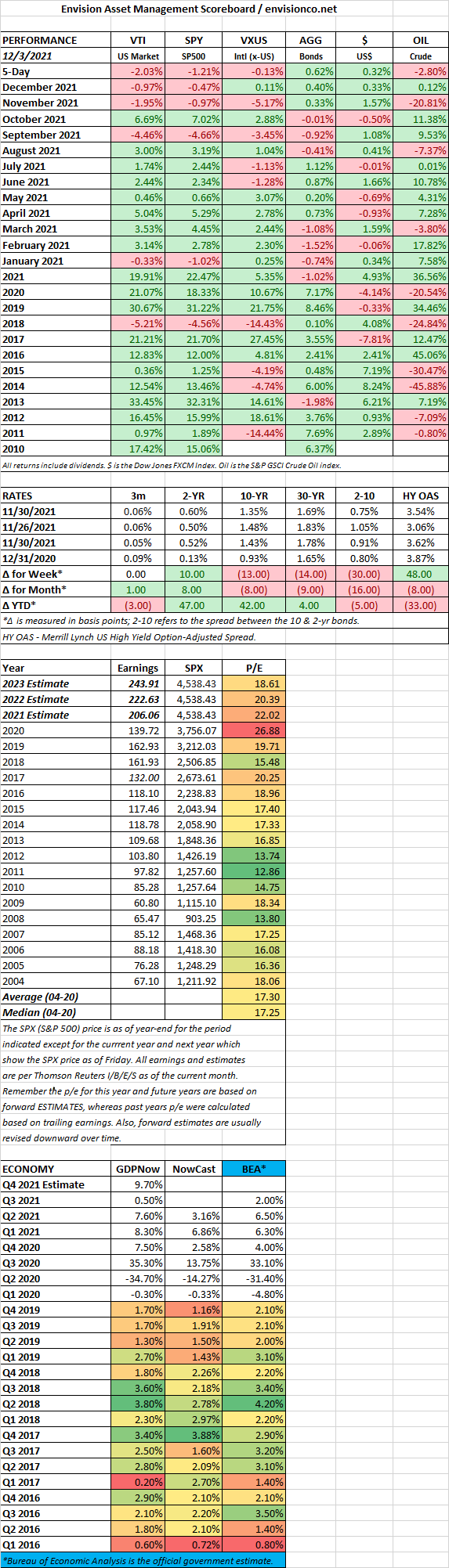

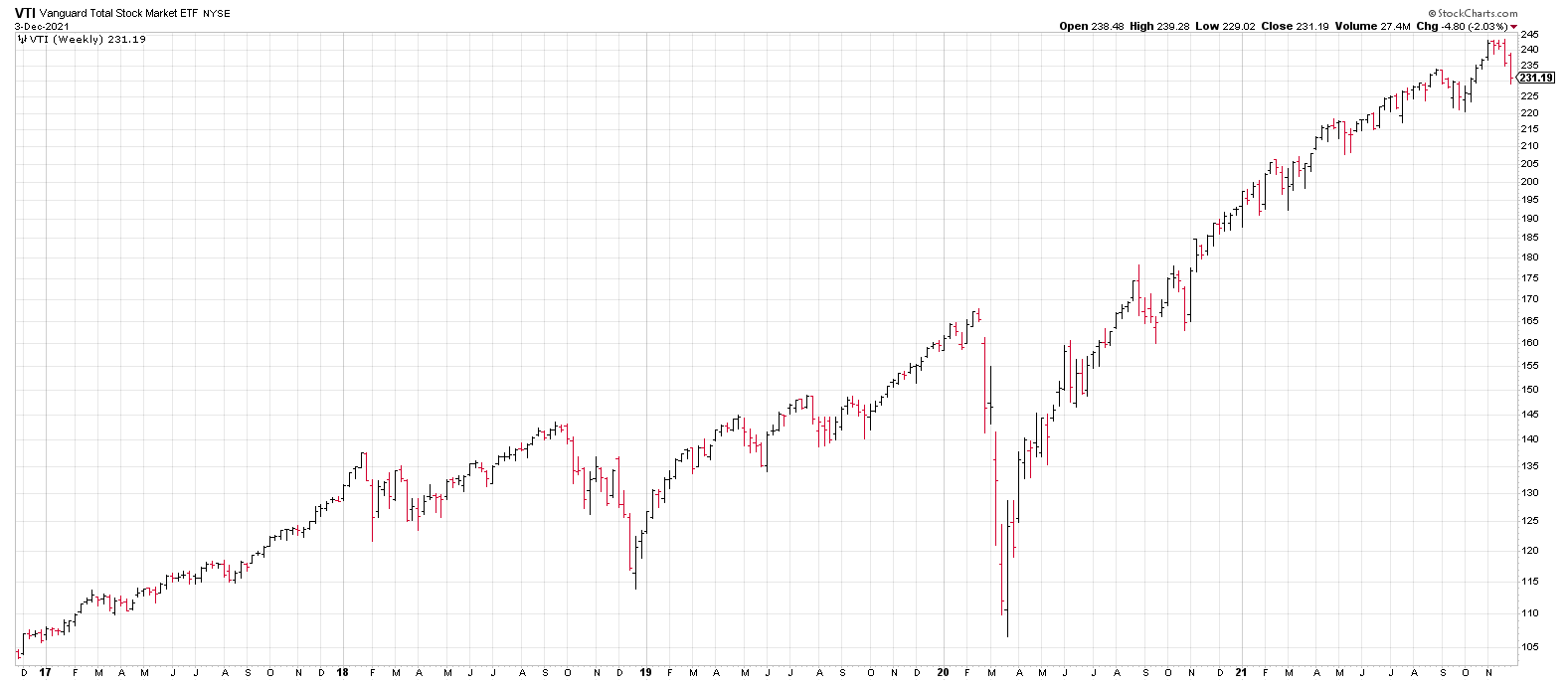

US stocks fell by 2.03% while international stocks were basically flat, off by 0.13%.US equities are now off by 4.77% from the November 8th high. The damage has been more extensive in small caps, the IWM is off by 11.55%. A lot of highflyers have been taking a big hit. Square is off by 37%, Paypal 40%, Docusign 56%, and Draftkings 60%. These are just some random samples. Blame the Omicron variant or an acceleration of the tapering, or both, either way, stocks and other risk assets have been selling off.

Bitcoin was down by as much as 35% on Saturday. The SPY, IWM, and bitcoin all hit their closing highs on November 8th. It looks more and more that the argument that bitcoin is a non-correlated asset with equities is nonsense.

Nonfarm payrolls were up by 210,000 in November, the lowest monthly growth of the year and off of projections of about 500,000. However, the report did have some good news. The household survey indicates that payrolls actually rose by 1.1 million, indicating that huge numbers are moving to self-employment. The unemployment rate fell to 4.2%, just above the Fed’s estimate of the natural rate of unemployment. 600,000 people returned to the workforce, increasing the labor-force participation rate to 61.8%, a new post-pandemic high. Average hourly earnings were up by 4.8% year-over-year. All of this indicates a tight labor market and will give the Fed the go ahead to speed up its bond-buying program and accelerate interest rate increases in 2022.

The overall economy is strong. GDPNow is forecasting 9.7% growth in Q4.

Long rates are falling while short-term rates are rising, meaning the yield curve has been flattening. The short-end is pricing in interest rate increases in 2022, while the long end is lower anticipating lower long-term inflation or slower growth or both.

SCOREBOARD